Powers Signal

A twice-monthly read of the moves between the great powers — eight powers, one signal.

covering ~6–20 June 2026 ~9 min read Subscriber edition

How to read this. We track the moves between the eight great powers — the United States, China, Russia, India, Japan, France, Germany, and the United Kingdom — across eight arenas of competition, from military force to trade, technology, energy, and diplomacy. Each arena gets a heat score from 1 (quiet) to 5 (very active) for the period, plus a trend arrow (▲ rising · ► steady · ▼ cooling). The edition leads with what moved, then traces how one power’s move pulls a response from the others. A map of who can pressure whom sits in the appendix at the end. Every claim links to its source.

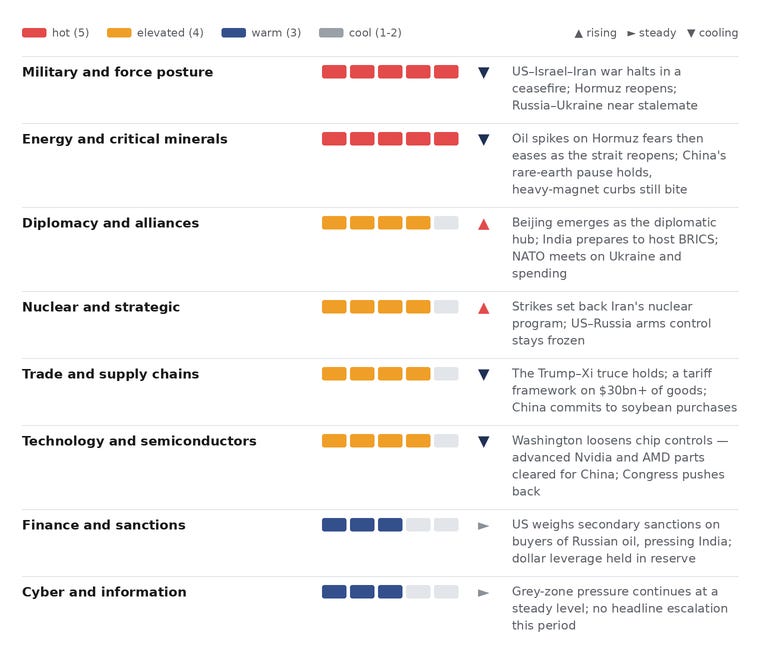

The read across the powers

This was a period of de-escalation — three confrontations cooled at once, but on terms set by the strongest hand at each table.

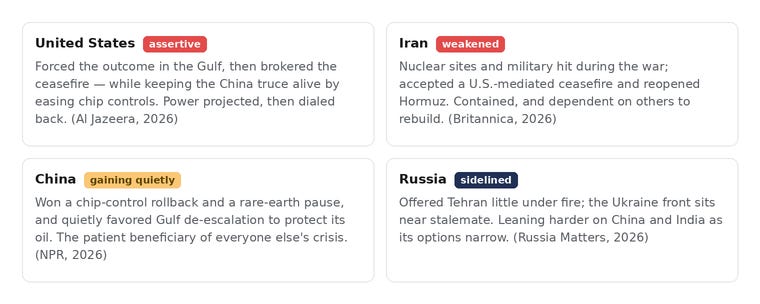

The largest move was peace, not war. After nearly four months of fighting, the United States brokered a ceasefire in the Iran war: a memorandum of understanding announced on 14 June and signed by the U.S. and Iranian presidents was set to end the conflict and reopen the Strait of Hormuz, and commercial traffic through the strait surged back almost immediately (Al Jazeera, 2026; RFE/RL, 2026). American force shaped the outcome; Russia, nominally Tehran’s partner, was a bystander.

The second move was a truce that held. The fragile understanding from the May Trump–Xi summit in Beijing carried through the period — and remarkably, it runs the other way from the last few years: Washington has been loosening its technology controls on China, not tightening them (East Asia Forum, 2026). In return, Beijing has paused its most sweeping rare-earth restrictions until November (Discovery Alert, 2026).

Underneath the calm, leverage hardened. China’s mineral pause has a fixed expiry. Washington is weighing sanctions on buyers of Russian oil — aimed squarely at India. And Europe kept converting fear into defense budgets. The guns went quiet; the pricing did not.

The heat map

Deep dive — the Iran war ends, and American force sets the terms

Washington brokers the ceasefire; Russia watches from the sidelines

The defining move of the period was the winding-down of the Iran war that had run since late February. A U.S.-mediated memorandum of understanding, announced on 14 June and signed by the American and Iranian presidents, set a path to end the fighting within sixty days and to reopen the Strait of Hormuz; within days, commercial shipping through the strait climbed sharply (Al Jazeera, 2026; RFE/RL, 2026). The war had already done lasting damage to Iran’s nuclear program and military, and had briefly threatened the world’s most important oil chokepoint (Britannica, 2026).

Read through the model, the striking thing is who acted and who did not. The United States supplied the force and then the settlement — the decisive party on both ends. China, the largest buyer of Iranian oil, had the most to lose from a closed Hormuz and the most to gain from reopening it; its interest quietly aligned with calming the crisis rather than prolonging it. Russia, Tehran’s nominal strategic partner, offered rhetoric but little material help — its attention and resources are pinned in Ukraine — and emerged visibly diminished as a security guarantor in the region (Just Security, 2026).

For a decision-maker, the takeaway is about reliability, not just oil. A power that cannot protect a partner under fire loses standing with every other partner watching. The Gulf states, and others who hedge between Washington and Moscow, just saw which guarantee held. The ceasefire is only sixty days old on paper; whether it hardens into a durable settlement is the first item on the watch list.

Deep dive — the US–China truce, and a technology reversal

Washington loosens the chip controls; Beijing pauses the mineral squeeze

The second thread is a de-escalation that surprises anyone who tuned out a year ago. Out of the May Trump–Xi summit in Beijing came a fragile truce that held through the period — and its content reverses the recent direction of travel. Washington has been relaxing its technology controls: a January rule cleared advanced Nvidia and AMD artificial-intelligence chips for sale to China and granted year-long approvals for U.S. chip-making tools, easing the squeeze that had defined the rivalry (East Asia Forum, 2026; Council on Foreign Relations, 2026). On trade, the two sides moved toward a reciprocal tariff-reduction framework on more than thirty billion dollars of goods, and China committed to large soybean purchases (NPR, 2026).

In exchange, Beijing postponed the sweeping October rare-earth controls — the ones that reached extraterritorially into products made with Chinese material — until 10 November 2026 (Discovery Alert, 2026). The catch: the April 2025 curbs on the heavy rare earths that matter most for high-performance magnets still apply, so the relief is partial (TechTimes, 2026).

Through the model this is mutual de-escalation — each side banking relief in the arena where it was most exposed, the United States in minerals, China in chips. But the leverage was paused, not surrendered. China’s mineral lever now carries a fixed fuse (10 November), and in Washington, Congress is advancing a bill to claw back a veto over chip-export licenses, which could reverse the executive’s softening. The chip-flow easing feeds directly into our sister brief, AI Signal.

Deep dive — the hedgers’ moment: India and Europe raise their price

While the giants pause, the swing states maneuver

When the great powers stop pushing, the middle powers move. India spent the past two weeks playing its multi-alignment hand to the hilt: preparing to host a BRICS summit that may draw both Xi Jinping and Vladimir Putin, banking a U.S. interim tariff cut that brought the rate on Indian goods down from a punitive level near 50% to about 18%, and at the same time deepening high-end defense and civil-nuclear cooperation with Russia (IMPRI, 2026; Valdai, 2026). The pressure point: Washington is weighing secondary sanctions on buyers of Russian oil — a finance-arena lever that would land hardest on India and China (Council on Foreign Relations, 2026).

Europe used the room differently — to rearm. After reforming its constitutional debt limit, Germany is on course to spend roughly €117 billion on defense in 2026, about 3.2% of its economy, with steeper rises planned through the decade (Atlantic Council, 2026). A NATO summit pressed members toward higher spending targets — a path the alliance has set toward 5% of economic output by 2035 — while again wrestling with Ukraine’s membership question under pressure from Washington (Ukraine War Analytics, 2026; Atlantic Council, 2026).

The through-line is the model’s core idea: when the strongest powers pause, the swing states use the opening to raise their price — India converting non-alignment into tariff relief and arms deals, Europe converting threat into permanent military weight. Neither is a great power in the old sense; both shaped the period.

Move of the month

How one American decision in the Gulf rippled through the strongest powers — and why China, not Russia, was the one quietly pulling for calm.

The chain shows why the response to an American move came through Beijing rather than Moscow. China buys the lion’s share of Iran’s oil and ships much of its energy through Hormuz, so a closed strait threatened China more than almost anyone — giving Beijing a direct interest in calming a war it did not start (RFE/RL, 2026). Russia, by contrast, had little to offer and something to gain from higher oil prices, leaving it on the sidelines. The signal: in this crisis, the decisive restraint came from the power with the most to lose downstream — exactly the kind of cross-power pull the model is built to trace.

Power movers

What to watch next

Whether the U.S.–Iran ceasefire signed in mid-June holds for its sixty-day term and turns into a durable deal on Hormuz and the nuclear program. (Al Jazeera, 2026)

10 November 2026 — when China’s suspended rare-earth controls are set to expire: do they return, get extended, or quietly lapse? (Discovery Alert, 2026)

Washington’s decision on secondary sanctions against buyers of Russian oil — the lever that would press India and China most directly. (IMPRI, 2026)

The U.S. Congress’s move to take back a veto over chip-export licenses, which could reverse the White House’s softer line on China. (Council on Foreign Relations, 2026)

Whether the Trump–Xi truce converts into the promised reciprocal tariff-reduction framework on $30bn+ of goods. (Atlantic Council, 2026)

Follow-through from the NATO summit on higher defense spending and Ukraine’s status. (Ukraine War Analytics, 2026)

Sources

[3] Encyclopaedia Britannica — “2026 Iran war,” 2026. britannica.com (accessed 20 Jun 2026).

Internal test edition. Material claims are verified to the linked sources as of 20 June 2026; several 2026 events remain fast-moving and dates may be revised in the live edition.

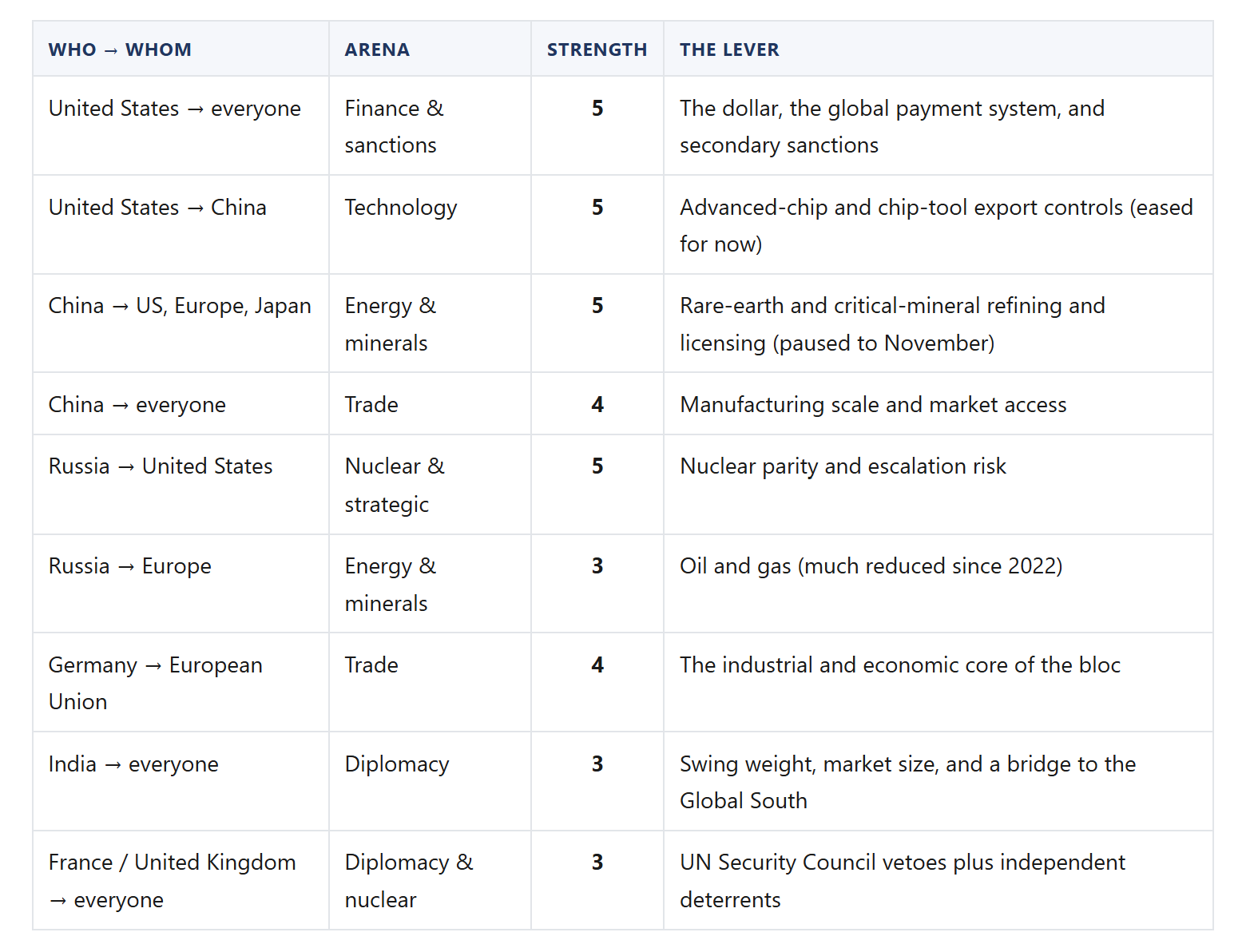

Appendix — who can pressure whom

The model’s relationship map, kept at the back as reference: the load-bearing levers between the powers, with the arena each runs through and a strength from 1 (minor) to 5 (decisive). This is the standing picture; the developments above are this period’s movements within it.

Powers Signal is a twice-monthly systems brief from The Critical Post. Method: the moves between eight great powers, scored for intensity and direction across eight arenas, with each move’s likely cross-power responses traced through an interaction model.

© 2026 The Critical Post.